Short-term opportunism vs long-term risk

Energy mix planning in the United States is being shaped by a confluence of factors. Growing load demand from data centers and advanced manufacturing, coupled with the need for reliability and affordability of electricity, is putting additional pressure on utilities and regulators. Recent changes to the Environmental Protection Agency’s (EPA) rules should not be overlooked or underestimated. For some utilities, these changes could materially alter the timing of coal plant retirements, especially where coal fleet retirements were already backdated prior to these changes. The EPA’s current deregulatory shift therefore carries significance not only for environmental compliance, but also for system reliability, resource adequacy, and long-term investment strategies.

Much of the market has focused on the increasingly negative outlook for renewables and what this means for energy mix planning, capital planning and the energy transition. However, relatively little attention has been paid to the consequences of the EPA’s deregulatory agenda for coal plant retirement dates. While these changes may not fundamentally alter coal’s structural decline, they do affect the pace and sequencing of retirements, which in turn could influence energy mix planning and short- and medium-term emissions trajectories. The EPA’s current deregulatory shift therefore carries significance not only for environmental compliance, but also for long-term investment strategies.

The EPA has embarked on a wide-ranging deregulatory initiative affecting coal-fired power plants. These rules touch on carbon emissions, air toxins, wastewater, coal ash and smog. For utilities and investors, this presents a dual narrative: near-term compliance cost relief for fossil-heavy utilities, but with heightened long-term uncertainty. While such changes may slow the pace of coal plant retirements, they are unlikely to reverse coal’s broader structural decline in the US, which has primarily been driven by deteriorating economics and operational efficiency relative to other sources of generation over the past decade. Compliance deadlines under existing rules largely fall between 2027 and 2032, yet the current administration has signalled plans to revisit many of these, aiming for more lenient standards.

Rule-making and changing: it’s complex

Changing EPA rules is a procedurally complex and time-consuming process, often spanning years and subject to legal review. Many deadlines under Biden-era rules were finalised only in 2024, and may not take full effect before another administration intervenes. This regulatory volatility complicates capital planning and long-term resource strategies. The current administration, however, has sought to bypass traditional processes by instructing agencies to suspend or halt enforcement of high-cost rules, such as tailpipe emissions and power plant standards. Rather than incremental adjustments, this approach marks a shift toward sweeping deregulatory action, with each review cycle expected to generate broader changes than before.

Greenhouse gas (GHG) emissions and the Endangerment Finding

Under the Biden administration, EPA rules imposed stringent carbon pollution standards, requiring Carbon Capture and Storage (CCS) or gas co-firing for coal and gas-fired plants. These requirements were generally treated by regulated utilities as outlier scenarios in their Integrated Resource Plans, given the uncertainty surrounding their enforceability owing to ongoing legal challenges. Instead of repealing these rules through the traditional process, the current administration has proposed overturning the 2009 Endangerment Finding, the legal foundation for federal greenhouse gas regulation. If repealed, this would dismantle the legal basis for emissions standards across the sector.

The near-term effect would be to remove costly CCS requirements, offering compliance cost relief for coal and gas plants, particularly in states without aggressive decarbonisation mandates. Yet this relief could come at the price of greater regulatory fragmentation, as states may choose to set their own rules. Multi-state utilities such as AEP and Duke Energy could face heightened complexity and political pressure as they balance disparate requirements across regulatory constructs and bodies.

It is also possible that large corporate customers seeking low carbon electricity may face higher Scope 2 emissions if utilities revert to more carbon-intensive generation. This could increase demand for renewable energy certificates (RECs) and PPAs with IPPs, potentially bypassing regulated utilities. While the repeal is facing significant legal challenges, litigation could delay its resolution until at least 2028, creating additional uncertainty within utilities’ typical investment planning horizons.

Mercury and Air Toxics Standards (MATS)

The MATS rule, strengthened in 2024, imposed tighter mercury and toxic emissions limits and required continuous monitoring. The current administration is proposing to roll these back, including granting temporary exemptions to dozens of coal plants until 2029. While such changes could save the power sector more than $1 billion over the next decade, utilities that delay compliance may face future legal and reputational risks.

Notably, some utilities have already stated that they prefer not to pursue extensions under shifting federal rules. One of the largest multi-utilities in the US explained that “responding to short-term regulatory oscillation is not within our or our customers’ long-term interests – we want to exit as soon as possible and this remains our long-term strategy.” This perspective reflects a commitment to long-term transition planning rather than short-term cost relief, underscoring how strategic direction can diverge from federal regulatory leniency. Still, for others, growing electricity demand from data centers and AI is being used as justification to extend coal plant operations, particularly where capacity margins are tightening.

Effluent Limitation Guidelines (ELGs)

Wastewater discharge rules, also tightened under the Biden administration, had established stringent discharge limits by 2029. Delaying compliance deadlines may ease near-term capital burdens but reintroduces uncertainty and the potential for litigation. In the past, utilities such as AEP and NRG have cited these rules as direct drivers of coal plant retirements, highlighting their materiality in planning decisions.

Coal Ash Residuals (CCR) management

Coal ash management rules, which had required the closure of impoundments and remediation of contamination, are now being weakened under a “cooperative federalism” approach, shifting oversight to the states. While this may reduce compliance costs for utilities, it also increases liability exposure, particularly in states with less stringent standards. Activism and shareholder litigation around coal ash remediation remain potent risks for utilities, alongside potential challenges from insurers unwilling to underwrite facilities operating under looser environmental standards that carry risk.

Coal retirement plans and energy mix planning

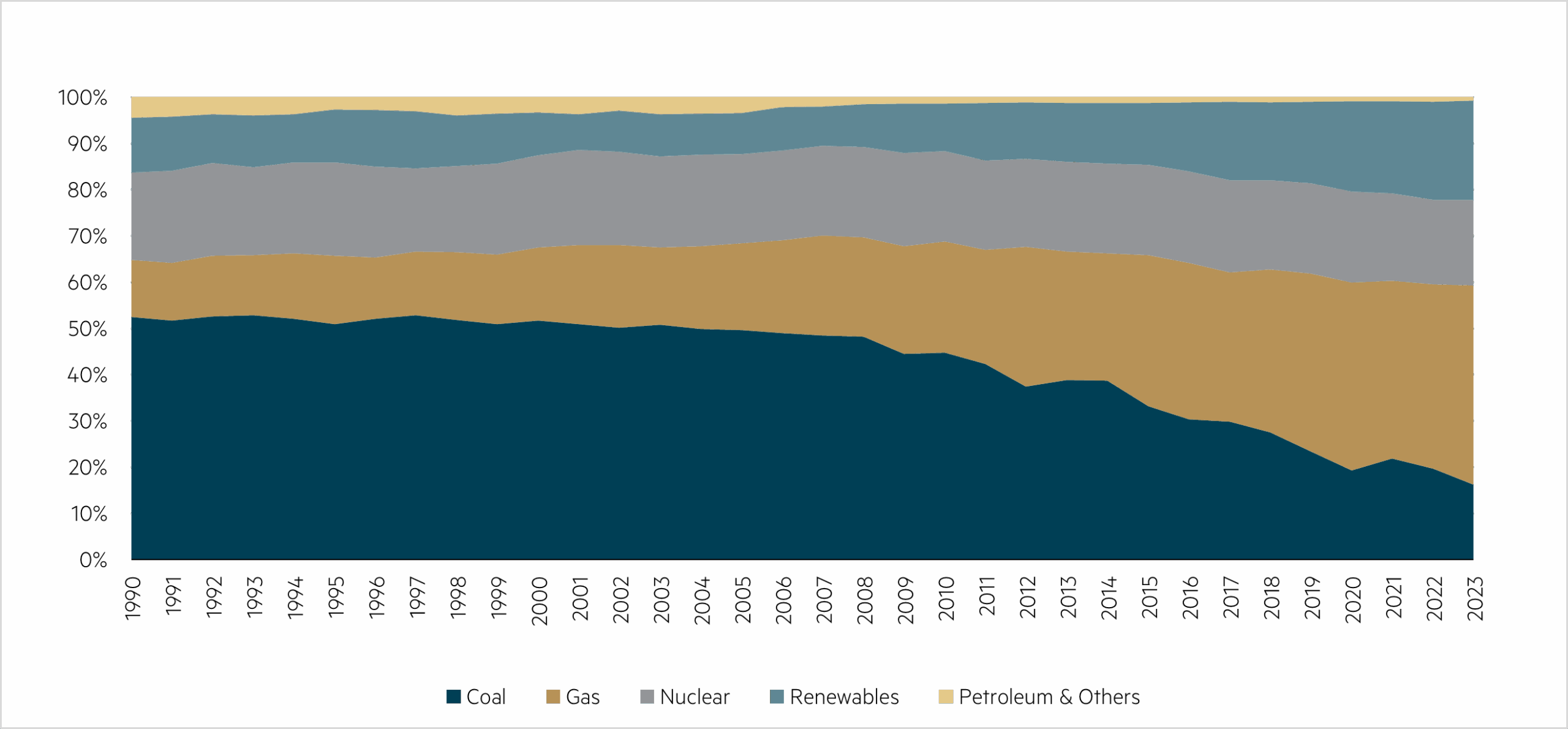

Despite the deregulatory push, changes in EPA rules are unlikely to be the sole factor delaying coal plant retirements. More pressing are the fundamental drivers of demand growth, affordability and reliability. Coal-fired electricity has already declined by more than half since 1990 and is expected to fall to around 5% of installed capacity by 2035.1 Retirements are dictated more by ageing infrastructure, lower efficiency, high costs and the superior economics of replacement technologies than by compliance deadlines alone.

US electricity generation mix (1990–2023)

Source: Energy Information Agency (EIA), US Electricity Generation Mix 1990-2023.

Source: Energy Information Agency (EIA), US Electricity Generation Mix 1990-2023.

That said, the rapid growth of data centers, electrification and reshoring of manufacturing are tightening reserve margins, leading some utilities to defer retirements for reliability reasons. For example, in May 2025, Evergy’s Integrated Resource Plan (IRP) outlined its plans to delay the retirement of ~914 MW of coal capacity across its Kansas Central, Evergy Metro and Missouri West subsidiaries. Equally the Department of Energy (DOE) has ordered CMS’s J.H. Campbell plant in Michigan to remain online longer than planned to preserve system reliability. The DOE estimates that keeping the Campbell plant online between May and June 2025 added approximately $29 million in costs for CMS’s consumers.2 These extensions, however, generally involve plants that no longer run frequently, limiting their broader impact on power markets. State public utility commissions, with their approval authority, often impose a more binding constraint on retirements than federal policy shifts.

Investor considerations

For investors, the deregulatory agenda should be seen as a temporary reprieve rather than a structural shift. Fossil-heavy utilities and independent power producers may enjoy short-term relief, but the medium-term is clouded by legal disputes, uneven state rules and planning uncertainty. Over the long run, risks of stranded assets, reputational harm and the potential reinstatement of stricter regulations are worthy of attention.

These regulatory changes may also affect utilities’ near-term emissions trajectories, potentially slowing progress toward emissions reduction targets. However, such effects may not truly materialise if a future administration reinstates strict standards that reverse the Trump administration’s approach. Utilities should be cautious about shareholder sentiment, as investors – especially in international markets – may respond negatively to the perception of these companies backsliding on decarbonisation commitments.

The enduring reality is that load growth, reliability and the relative economics of replacement technologies – not federal deregulation alone – will continue to shape the pace of coal retirements and the future energy mix.

1 Energy Information Association (EIA), Morgan Stanley Research estimates, June 2025.

2 Utility Dive, ‘FERC approves cost allocation paths for power plants DOE ordered to run past shutdown dates’ (August 2025) .

Georgia

Interested in investing with us?